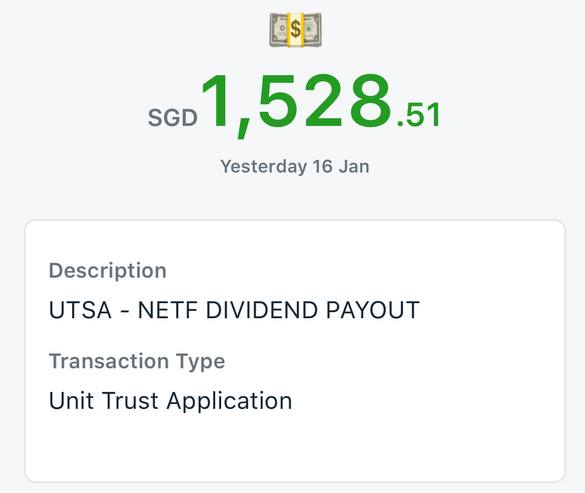

Feeling really happy with my investing journey and the results so far! 🎉 Just two days ago, I received a dividend payout of SGD 1,528 from my Unit Trust investments—my single largest payout yet! This marks another step in building my portfolio, and seeing these results keeps me inspired to stay consistent.

Back in January 2024, I received SGD 1,055, and by July 2024, the payout grew to SGD 1,252. It’s incredible to witness the compounding effect in action!

Currently, I hold roughly 17k++ units, and this milestone reminds me that every small decision to invest adds up over time. The journey is far from over, but I’m motivated to keep growing my portfolio and achieving greater financial goals. Here’s to more learning, persistence, and of course, dividends! 💪📈

#KopiLui #DividendInvesting